Issue 25: The Bill Comes Due

Apollo crossed $1 trillion. Blackstone hit its largest redemption request ever. Big Tech is spending $725 billion and the debt markets are the first place it lands.

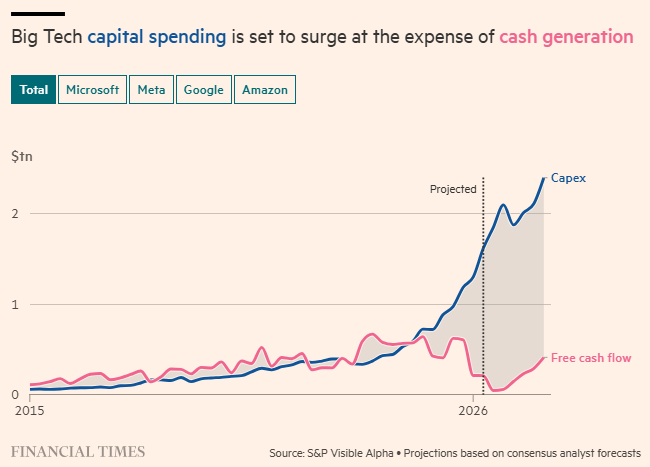

Four companies decided this year to spend $725 billion building AI infrastructure. Amazon. Alphabet. Microsoft. Meta.

That number is real. It is more than the GDP of Switzerland. In a single year. And when you spend $725 billion, you have to get it from somewhere.

You borrow. You issue debt. You pull cash from every corner of the balance sheet. And that money has to come from markets that everyone else is also trying to access.

This week, two things happened in private markets that most people did not connect to each other. Apollo crossed $1 trillion in assets under management and quietly announced it is moving toward daily pricing for private credit assets. And Blackstone disclosed that investors tried to pull 7.9 percent of assets from its $82 billion private credit fund — the largest redemption request in the fund's history. Blackstone met every dollar of it. But the request is the tell.

The people who moved money into private credit expecting stable, uncorrelated yield are watching the AI capex cycle run through the debt markets and doing the math. Daily pricing from Apollo is not a routine update. It is what you offer when the institutional world starts asking how liquid their illiquid assets actually are.

This is what private markets are doing right now. The S&P chart is the distraction. This is the story.

Five things this week. Plus a personal note from Las Vegas at the end.

$725 Billion In. The Private Credit Market Feels It First.

The four hyperscalers — Amazon, Alphabet, Microsoft, Meta — are spending $725B on AI capex this year. Their combined free cash flow is on track for $4 billion. Not each. Together. That's the lowest since 2014, when revenues were one-seventh of today's size.

Amazon is tracking toward a net cash outflow of $10 billion for the year. Microsoft says tariff inflation is adding $25 billion to its capex. Meta raised its forecast and kept raising.

When companies this size run near-zero free cash flow, they tap debt markets at scale. That issuance competes for the same institutional capital that funds private credit. Spreads compress. Deal terms tighten. The stress shows up in redemption requests before it shows up in headlines.

The Financial Times broke the capex analysis. Read it here. The article is behind a paywall (I usually avoid paywalled links), but FT's current $1-for-four-weeks promo makes it well worth the read. Apollo's $1 trillion milestone and daily pricing move (free to read): here.

Stop Sending Your Pitch Deck

Investors spend an average of 3 minutes 44 seconds on a cold deck — spread across 22 slides. That is 10 seconds per slide if they make it through. Most do not make it through. There is a sequence that works better. Send a teaser. Get the meeting. Walk the deck live. Let your Deal Box deal link handle the follow-up intel.

Read it: Stop Sending Your Pitch Deck.

How to Pick Your Pre-Seed Valuation

Most founders either guess or copy a number they heard at a demo day. Neither works when an investor pushes back. The framework: work backward from runway and dilution, account for your background premium, know who you are raising from, and pick the number you can actually close. A clean round at $7M beats a stalled raise at $12M every time.

Read it: How to Pick Your Pre-Seed Valuation.

The Investor Onboarding Problem

Getting investors through accreditation, compliance docs, and subscription agreements manually takes weeks. It becomes a full-time job at exactly the moment you cannot afford one. We built the platform that handles it. If you are in the middle of a Reg D raise and want to see how it works, book 20 minutes here. (We are not a broker-dealer. Zero transaction fees. We earn on technology and advisory services provided to issuers only.)

6 Retailers, 6 Bankruptcies, 0 Refunds.

In 2005, a private equity operator wrote a memo with a shopping list. Lord & Taylor. Hudson's Bay. Saks Fifth Avenue. Galeria Kaufhof. Neiman Marcus. He wanted to buy them all.

He bought every single one.

Every single one eventually filed for bankruptcy.

The last deal merged Saks and Neiman Marcus and convinced Amazon to put in $475 million. Amazon has since said its investment is, in its own legal filing, "presumptively worthless."

Saks Global filed for Chapter 11 in January. The rest of the luxury retail market is growing.

There is a lesson in there for anyone structuring a deal right now. A track record of buying things is not the same as a track record of building them. The fees cleared on every transaction. The companies did not.

A Note From Las Vegas

I spent two days at Bitcoin 2026 the week before last. The Venetian. Forty thousand people. Six stages. Five hundred speakers.

The most consequential thing that happened had nothing to do with where Bitcoin closed on Tuesday. The SEC Chair showed up for the first time in conference history. The CLARITY Act passed the House 294-134. A tokenization sandbox for real-world assets now exists. I wrote the full piece here — worth reading if the regulatory architecture for private markets matters to you.

The AI capex story and the private markets story are the same story right now. When the four largest companies on earth are running near-zero free cash flow to build infrastructure, the capital that used to fund early-stage companies is going somewhere else. That is the environment you are raising in.

More next Friday.

Thomas Carter

Chairman and CEO

Deal Box

May 8, 2026 · O‘ahu