Issue 28: Tokenization, So Far

We pulled the live numbers. The leaders aren't who you'd guess, and the thing everyone wants isn't there yet.

Tokenization gets described as the future of finance. It is worth looking at what is actually tokenized today. We pulled the live numbers this week, and they are smaller, more concentrated, and stranger than the narrative suggests.

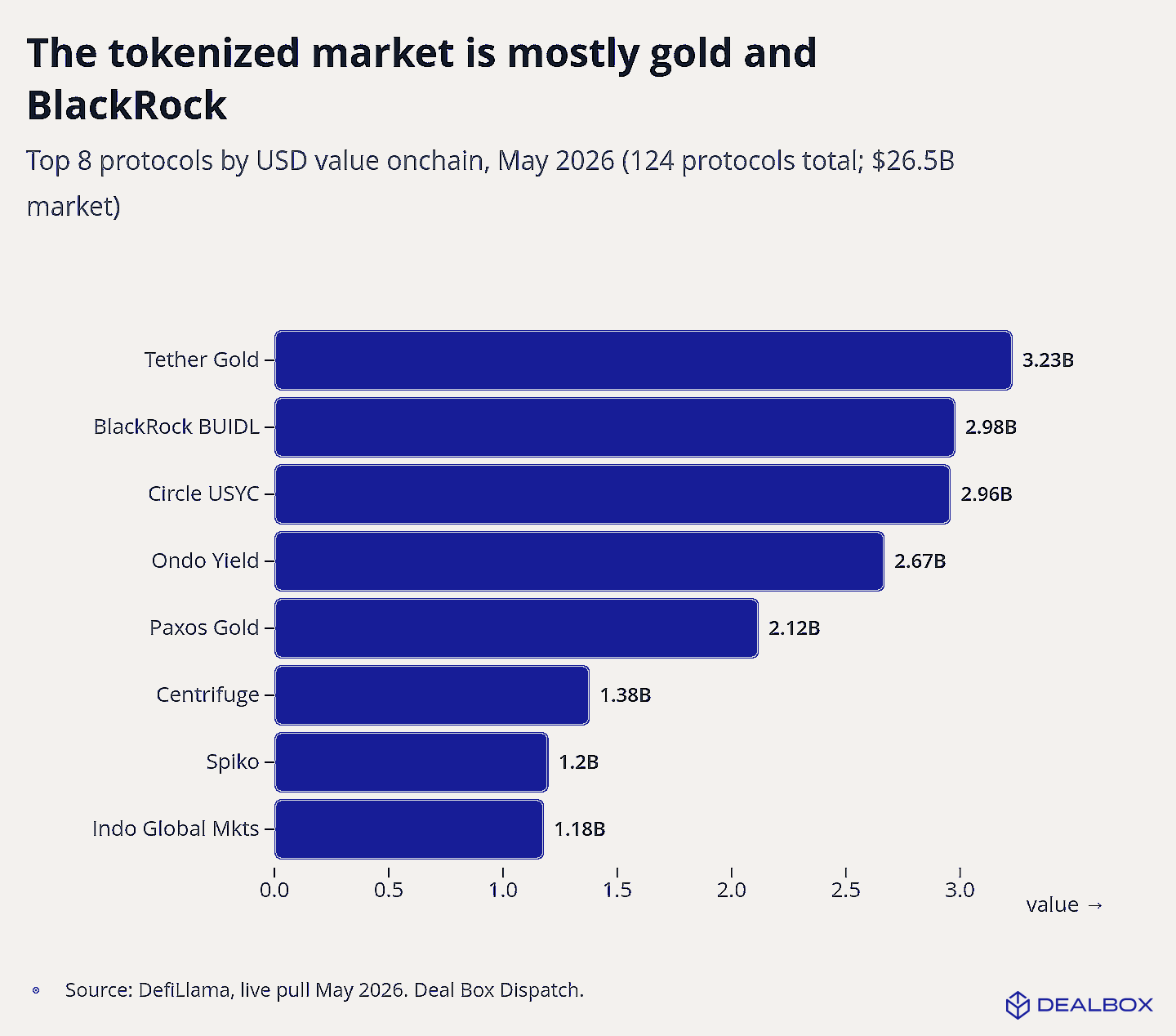

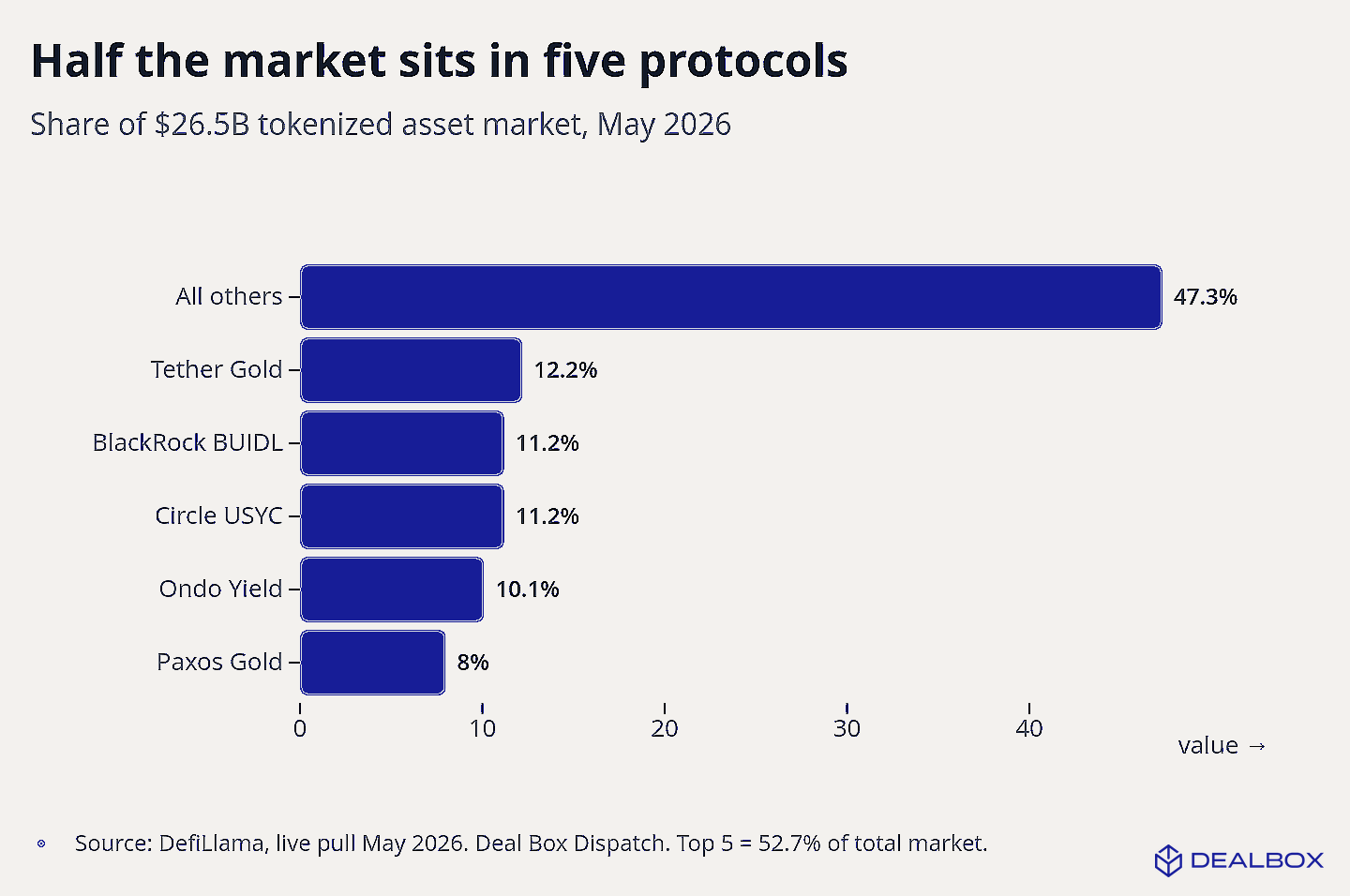

The whole tokenized asset market is 26.5 billion dollars across 124 protocols. That sounds large until you set it against the markets it is meant to replace, where it still rounds to almost nothing. The current leader is not a bank and not a crypto startup. It is tokenized gold. Tether Gold and Paxos Gold together hold more than 5 billion dollars. BlackRock's BUIDL fund sits second at around 3 billion, already live on three chains including Aptos. And the market is concentrated. Five protocols account for 53 percent of it.

The more interesting thing is what is missing

Tokenized equities barely register. Real ownership of real companies onchain, the thing both retail and institutions say they want, sits near 1.5 billion dollars. That is about a thousandth of a percent of the shares it tracks. (The figure is from a16z's Robert Hackett.) The appetite is large and the actual issuance is almost nothing. That gap is the story.

You could see the appetite clearly this week

A developer called Trade.xyz launched a SpaceX pre-IPO contract on Hyperliquid on May 18, built on its HIP-3 framework. It traded 33 million dollars on the first day, and the chief executive of ICE, which owns the New York Stock Exchange, suggested the market might end up bigger than Nasdaq. It is worth being precise about what this actually is. Trade.xyz holds no SpaceX shares. The contract is a synthetic perpetual, a leveraged bet on a price, with no ownership and no shareholder rights. When it fell 45 percent on May 28, what unwound was leverage, not equity.

The demand is not in doubt

People will take a leveraged bet on a company they cannot legally own, and they will do it by the millions. What does not yet exist, at any real scale, is the formation layer. The place where a genuine equity comes into existence onchain, with real ownership, under US regulation, where the capital reaches the company rather than a perpetual pool offshore. Trading a name and forming capital are different activities. The first one is busy and visible. The second one is mostly still to be built, and it is the part we work on.

The Latest in Private Markets

- The Fed looks more like a rate hiker than a cutter. J.P. Morgan’s Cembalest: labor market tightness, manufacturing price pressures, and the output gap all align more closely with historical rate-hike conditions. Monetary policy rules point to an optimal range of 4.00–4.85% versus the current 3.50–3.75%. (source)

- AI productivity is flashing a 57% signal. A San Francisco Fed model gives a 57% probability the US has entered a high-productivity-growth regime, mirroring 1997 pre-surge readings from the 1990s tech boom. Labor productivity is already 8 points above 2022 levels. (source)

- The renminbi just crossed 80% of China’s trade finance. Up from 20% in 2020. The dollar has been displaced as the dominant currency in Chinese trade credit in under five years. (source)

- BlackRock is picking rails. BUIDL now runs on Ethereum, Solana, and Aptos. When the largest asset manager spreads across chains, that is institutional money choosing infrastructure. (source)

- What a zero-fee platform actually costs. The fee question worth asking before you wire. (read)

One thing to do

If you want to see what capital formation looks like when the equity is real and the ownership is yours, the portal walkthrough is here: book a 20-minute walkthrough.

(We are not a broker-dealer. Zero transaction fees. We earn on technology and advisory services provided to issuers only.)

A note from Oahu

I am writing this from Honolulu, where it rained most of the week.

I had a call Thursday with someone who has spent his career moving between the physical world and capital markets... military, then government, then private. He just got back from two weeks in Europe. Part of what he is working on: finding sources of titanium that do not run through China, because the supply chain for certain defense applications depends on it.

I kept thinking about that conversation while pulling the numbers for this issue. The reason gold leads the tokenized market is not complicated... it has been a portable store of physical value for five thousand years, and the custody story is cleaner than almost anything else. The reason someone is hunting titanium in Finland is the same reason. Physical scarcity is the underlier. The tokens, the contracts, the synthetics run on top of something real.

Most of what gets written about this space is about the digital layer. The physical layer is where the actual work is happening.

More to come next Friday.

Best,

Thomas

Honolulu, Hawaii | May 29, 2026

The Deal Box Dispatch is published weekly every Friday. Deal Box operates as a Title II matchmaking platform under the JOBS Act Section 201(c) exemption, with zero transaction fees. We are not a broker-dealer. We earn on technology and advisory services provided to issuers only. Nothing in this newsletter is a recommendation, solicitation, or offer to buy or sell any security.