Issue 26: Nobody Has Ever Grown That Fast

Nobody has ever grown that fast.

Everyone is pricing a number. Almost nobody checked whether the number has ever happened.

Here is the number.

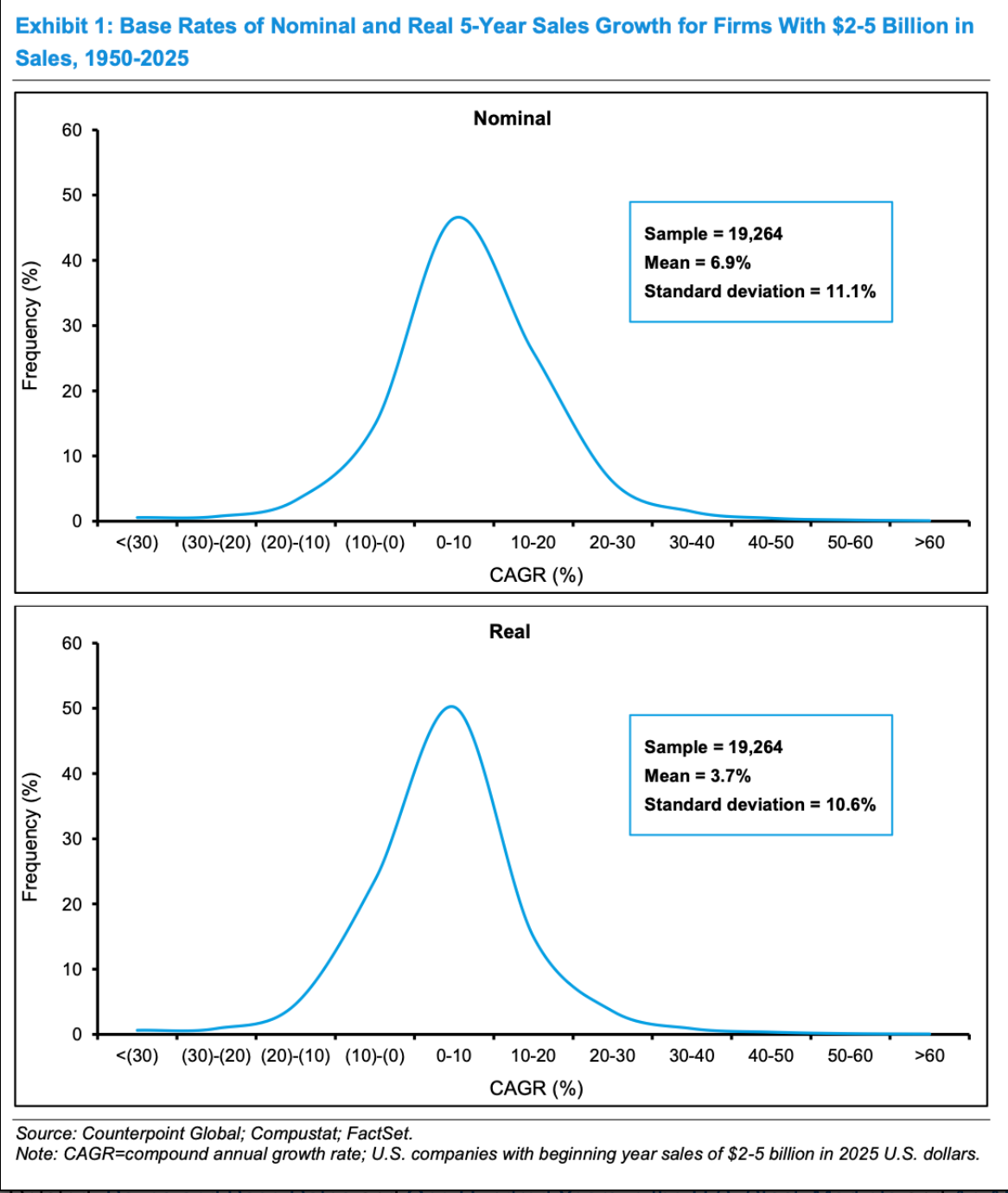

The leading AI company did $3.7 billion in sales in 2024. The forecasts in the press put it at $184 billion in 2029. That is a compound growth rate of 118 percent a year, for five years straight. Michael Mauboussin and Dan Callahan at Morgan Stanley, surfaced this week in Ed Conard's Macro Roundup, did the obvious thing almost nobody does. They checked it against history. They pulled every five-year sales growth rate for every US public company from 1950 to 2024, about 18,900 of them, and looked for one that had ever grown that fast from sales that large. They did not find one. Not a single company, in seventy-five years.

The forecast is not aggressive. It is unprecedented, in the literal sense of the word. A large part of the market is being priced off a growth rate that has happened exactly zero times in the entire record.

Three things this week. Plus a note from Honolulu at the end.

Nobody Has Ever Grown That Fast

The number got worse after they wrote it down.

When Mauboussin ran the first cut, the press had the company at $145 billion in 2029, a 108 percent annual growth rate from 2024. Before the ink dried, the projection was revised up to $184 billion. That is 118 percent a year. Then take the next data point. The company reportedly did $13.1 billion in sales in 2025 and forecasts $284 billion in 2030. That is an 85 percent compound rate over five years. Run it against the same 18,900 companies and you get the same answer. No company has ever grown that fast from a starting point that large.

This is not a piece about whether AI is real. It is real. This is about what every other valuation in the market is now quietly leaning on.

When the largest companies are priced off a five-year path that has no precedent in seventy-five years of data, that price does not stay in one stock. It sets the comp. It sets the multiple the next AI round prices against. It sets what a founder three layers downstream thinks their own company is worth, and what an allocator thinks they have to pay to get in. Everyone is doing the same arithmetic off the same number, and the number has a base rate of zero.

You do not have to call the top to take the lesson. The lesson is older than this cycle. A forecast is not a fact. A story priced like a certainty is the most expensive thing you can own, and the most expensive thing you can underwrite. The founders and investors who come through this fine will be the ones who can tell the difference between a number that is real and a number that is narrated.

For founders and allocators right now. When the comp is built on something that has never happened, the only thing you control is whether your own numbers are the ones that are real.

The Five Traits Every Founder Who Closes Has

I have watched several hundred founders try to close a raise since 2000. Two of my own companies went public. Seventy-five companies went through Deal Box. Most founders do not close. The ones who do share five traits, and the surprise is not the traits. It is how few founders show them where it matters, which is in the materials, before the first call.

Obsession is a track record, not a passion. Coachable is not agreeable. Honesty is a clock. Selling is closing, not charisma. And hiring smarter than yourself is the leverage test. Investors run that audit on your deck, your data room, and your model before they ever take the meeting. By the time you are in the room, the decision is mostly made.

I wrote the whole thing down, including how each trait shows up in the work and the one-question audit to run before your next meeting. Read it: The Five Traits Every Founder Who Closes Has.

If you want those materials to do the talking for you, that is what we build. (We are not a broker-dealer. Zero transaction fees. We earn on technology and advisory services provided to issuers only.) Package your raise with Deal Box.

The Pot That Was Too Good to Sell Twice

Cornell Capital bought Instant Brands, the company that makes the Instant Pot, and rolled it together with the maker of Pyrex.

It was the right kind of product. Everybody wanted one. During the boom, everybody bought one.

That was the problem.

The Instant Pot does not break. It does not wear out. It does not have a model you need to upgrade to every two years. So once the people who wanted one had one, there was no one left to sell the next one to. A beloved, durable, do-one-thing-perfectly product is a wonderful thing to own and a hard thing to put on a leveraged balance sheet that needs the next quarter to be bigger than the last. Instant Brands filed for Chapter 11 in 2023.

There is a lesson in there for anyone structuring a deal right now. Durability is a virtue in a product and a liability in a financial model that assumes everyone comes back. Before you underwrite the growth, ask the unglamorous question. Who buys the second one. If the answer is nobody, because the first one was too good, you do not have a growth problem. You have a debt problem wearing a growth costume.

Also, RIP to the company that got killed by making something people loved enough to keep.

A Note From Honolulu

I have been in Honolulu, and most of my week has been founders, not capital.

There are more real builders out here than the map would tell you. People with revenue, a product that works, and a clear reason to raise, who happen to be six time zones from where everyone assumes the money sits. I have spent the week with potential issuers across the island. Almost none of them are pricing themselves off a story. They have actual numbers, and the numbers are smaller and far more believable than the ones in the headlines, which is exactly why I would back them.

That is the through line this week. The market is busy underwriting a growth rate that has never happened. Meanwhile there are founders with growth that did happen, sitting outside the hubs, getting overlooked because their number is real and therefore boring next to the one that is narrated.

A founder with a true number and an investor tired of paying for a story do not need to be in the same city. They need the same link. The thing that has always closed a raise is not the biggest forecast in the room. It is the one that holds up when someone checks it.

More next Friday.

One last thing.

If you know a founder with a real company and real numbers, doing everything right and getting drowned out because they are not the loudest logo in the cycle, forward this. Reply with their name. If they launch a portal with us, I will send you a thank-you you will actually want.

And if you want to see what we built, go to dealbox.io and click Get Started. Pull up. Show me what is broken. We will fix it.

Thomas Carter

Chairman and CEO, Deal Box

Honolulu, HI

May 15, 2026

The Deal Box Dispatch is published weekly every Friday. Deal Box operates as a Title II matchmaking platform under the JOBS Act Section 201(c) exemption, with zero transaction fees. We are not a broker-dealer. We earn on technology and advisory services provided to issuers only. Nothing in this newsletter is a recommendation, solicitation, or offer to buy or sell any security.